What are the trends that impact your company’s planning process and how to transform it to be more effective?

Introduction

Having a strategy is fundamental to the success and survival of any organization. However, the strategic planning process is one of the least wanted in most companies. Executives criticize him for being long, boring, complicated and ineffective. Even more serious, many see it as inappropriate for a world that changes more and more rapidly. In this document, we examine the trends that have made the traditional way of doing strategic planning obsolete and propose ways that you can improve the development of strategies that will allow your company to compete in the new digital and knowledge economy.

Companies face an ever-changing, increasingly complex business environment, which they need to transform

We live in a business environment that is changing rapidly. Globalization, demographic changes, policies and emerging technologies are creating a more volatile, uncertain, complex and ambiguous environment (VICA) [1] in which companies must compete. Exponential technologies, such as artificial intelligence, the cloud, the internet of things and blockchain, among others, are causing dramatic changes (disruption) in most industries, now known as the Fourth Industrial Revolution.

New generations of customers and consumers have new expectations and needs that are very different from those of their predecessors. The new competitors come from other industries or are startups that attack with radically different business models.

Faced with this scenario, companies need to transform and be more agile and adaptable in order to remain relevant in the future and survive. In fact, 85% of the executives surveyed worldwide think that they need to transform their companies, due to changes in their surroundings and their markets, and 69% consider that their companies are not changing as fast as the market (Innosight [2]).

In addition, 72% assure that their business models will be threatened in the next 3 years (Palladium [3]) and 41% indicate that their companies will become a completely different entity in the next 3 years (KPMG [4]).

Strategic planning is becoming increasingly challenging

When asked about their perception of strategic planning processes, 63% of the executive segment say that strategy formulation is more challenging than 10 years ago and 74% think it is taking longer than a decade ago (AT Kerney [5 ]). 86% of CEOS say they have little personal time to think about the disruption and innovation forces that affect the company’s future, and the majority are concerned about their customers’ low loyalty.

70% of CEOs are concerned with the number of issues that are critical to their organizations and for which they have little personal experience, such as new digital technologies and disruption (KPMG [6]). 42% of executives consider that the cycles of strategic planning have been reducing in recent years (A.T. Kerney) and only 14% recognize that they update their strategies regularly, according to the changes in the market (Palladium [7]).

The lives of companies and their strategies have been reduced

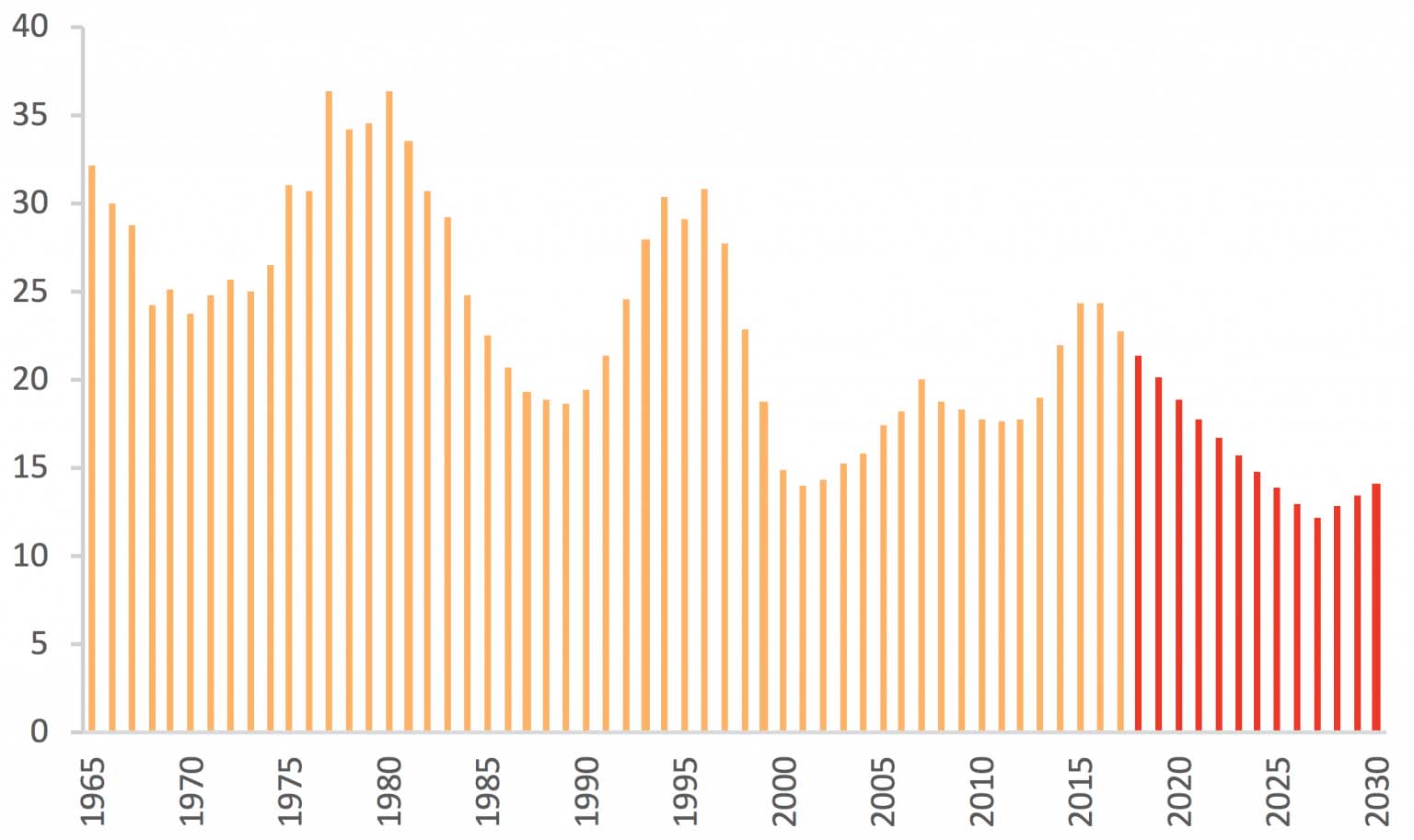

Due to the changes mentioned, the lives of companies, their strategies and the probability of survival have been significantly reduced in recent years. According to a study published by Innosight, the average life of the companies that make up the indicator of the 500 largest of Standard and Poor’s 500 (S&P 500 [8]) decreased from 33 years in 1964 to 24 years in 2016 and is expected to reach only 12 years in 2027 (half of that presented in 2016). This means that, with this exit rate, half of the companies in this index will be replaced in the next 10 years.

Average life of a company in the Standard & Poor’s 500 (S&P) Index

Today, more than ever, companies need to devote time to define their strategy. However, the strategic plan becomes irrelevant and obsolete in the blink of an eye and organizations are having to enter new cycles more often to rethink themselves. Strategic planning must be a continuous and frequent process, which cannot be postponed until the end of each year, as competitors will not wait for their annual strategy review process to attack. Nor will customers expect their annual strategy cycle to change their preferences, and technology will not wait for their annual meeting to make their company obsolete.

In her book The End of Competitive Advantage, Professor Rita McGrawth suggests that sustainable competitive advantage no longer exists and that today we can only wish to have temporal advantages [9]. The key to the new temporal advantages lies in the ability to adapt to environments that are constantly changing and difficult to anticipate. Today’s strategies must be more agile and flexible.

Future strategic planning should produce a portfolio of temporal advantages that are dynamically reviewed. The strategy should be a living document that is constantly being revised and companies are forced to improve their ability to get out of business quickly where they have lost their competitive advantage.

Companies are dissatisfied with traditional approaches to strategic planning

According to global surveys, 50% of executives believe they do not have a winning strategy (Strategy & [10]) and 90% are missing opportunities in the market due to an inadequate strategy (IBM [11]).

Although 61% consider the quality of their strategy to be good (Palladium), only 33% say that their strategies rest on new data and insights, which are not available to their competitors (McKinsey [12]). Only 53% of executives say their strategies emphasize creating a competitive advantage over their competitors. The rest indicate that their strategies could describe how to pursue the adoption of industry best practices and achieve operational improvements (McKinsey).

The traditional way of doing strategic planning is obsolete

Despite the new environment they must face, the way companies carry out their strategic planning has not changed in many years. We continue to use tools created in the 1970s to design strategies for the 21st century. We continue to develop five-year strategic plans for the knowledge and digital economy, which become obsolete the moment they are printed on paper. The following summarizes the fundamental challenges of current methods for strategic planning.

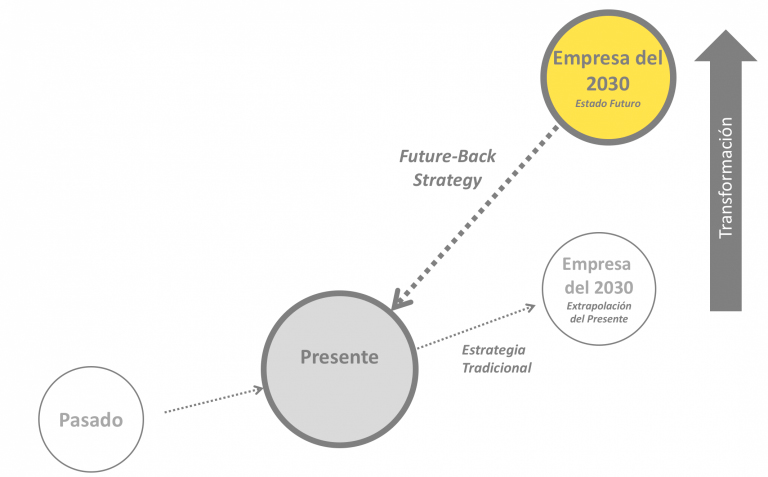

Companies project the past into the future and believe that the factors that made them successful in the past will make them successful in the future

The way in which the vast majority of companies carry out their strategic planning is through the analysis of data from the past. This leads them to fall into the trap of projecting a future as an extrapolation of the present, which generates only incremental strategies, that is, doing more of the same in the markets in which they already participate. What companies should do is create a vision of the scenario in which their company must compete and then develop a future-back strategy to identify the changes they have to make in order to transform and compete in that future.

Future-Back Strategy

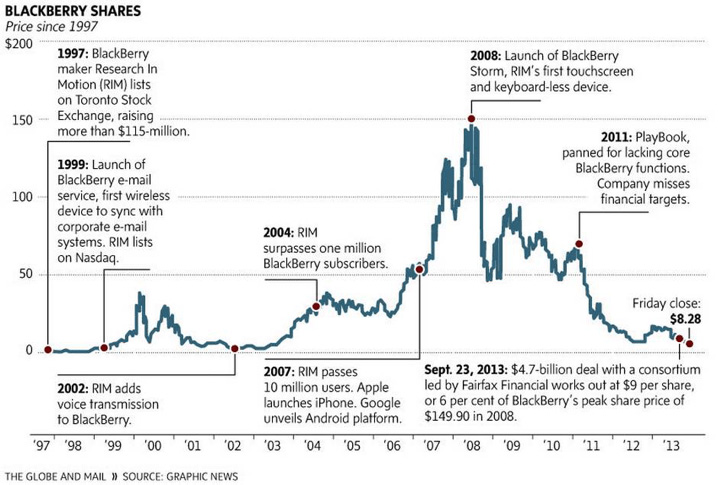

What companies did not realize is that, in the current scenario, their competitive advantage will disappear and the facts that made the strategy successful in the past are not necessarily the same that will make it successful in the future. That is why the incremental focus of the strategy has a high risk for companies that are in the industries where inflection points will occur with the potential to change the rules of the game. Such was the case with the company RIM, which produces the Blackberry phone, which lost its competitive advantage and its value shortly after the launch of the Apple iPhone in 2007.

RIM share value after the iPhone launch in 2007

Companies confuse strategy with planning

Surprisingly, many companies think that it is tantamount to making the strategy the definition of strategic objectives, initiatives and activity plans that end in a budget for the next year. This shows a lack of knowledge of what strategy really means. A plan is not the same as a strategy because strategy is about making decisions and making resignations.

It is easy to make a list of initiatives to keep doing more things, in the same markets and with the same customers, without giving up anything, but this is a safe recipe for mediocrity. No company has the resources or the time to be good at everything.

According to Michael Porter, “strategy is the set of choices that define a company’s distinctive approach to compete and the competitive advantages on which it is based. The Strategy means creating a unique competitive position that implies doing different things to deliver a unique value to customers ”.

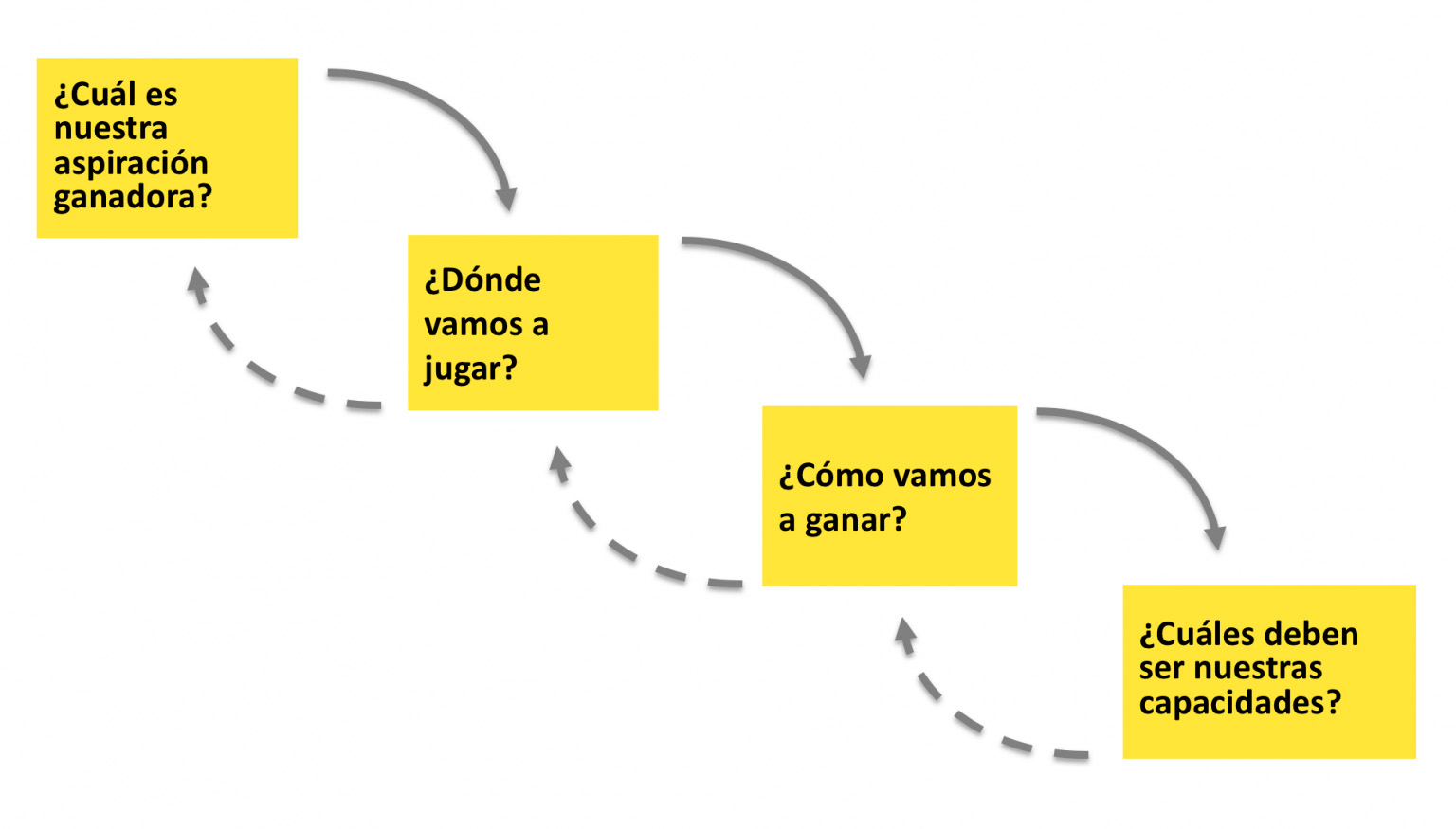

Companies believe that they have a strategic plan because they have defined that they want to achieve a certain level of growth or execute several projects for the following year, without realizing that they have not answered the key questions that must be answered in a strategic planning process:

- What is our winning aspiration? Decide what it means for the company to gain competitiveness vis-à-vis customers in order to capture the highest possible profitability.

- Where are we going to play? Define the geographic region, market segments, with what type of products and through which channels you will compete.

- How are we going to win? Decide the value proposition that will differentiate the organization from its competitors.

- What skills do we need to win? Decide which capacities you will bet on in order to obtain a long-term competitive advantage.

The strategic decision ladder

The challenge it imposes on the strategy is that these decisions have to be made in an integrated way, so the arrows down and up in the top image. That is, you cannot decide that we are going to compete in a given market without having the tools to win in it or not having the capabilities to support the chosen competitive advantage.

Believing that the company’s strategy will come out of a SWOT

The favorite tool in the strategic planning process is SWOT (Strengths, Opportunities, Weaknesses and Threats, in English). Although this tool is very popular and easy to use, companies have not realized that it does not help to produce relevant or innovative strategies. The problem is that there are no generic strengths or weaknesses; they exist only in terms of the choices that must be made.

For example, the company Blockbuster, in its SWOT analysis, may have defined that its chain with more than 11,000 physical stores was a STRENGTH, without realizing that in view of the changes that would happen in their industry they were more of a WEAKNESS. Like SWOT, many companies use tools that were invented many years ago and are obsolete in the current context to make their strategic plans.

Believing that the strategy analysis unit is the industry in which it competes

The traditional approaches of strategy take as an analysis unit the industry in which the company competes, this is justified by the fame that took approaches like the “Five Forces of Porter” for the analysis of an industry. However, digital technologies have blurred the boundaries between industries and a focus on “industry” may not be the most appropriate.

For example, car companies like Ford and General Motors are no longer competing against similar companies, if they are not competing against technological leaders like Tesla, Uber and Google (through their self-driving cars division). In the new mobility playing field, these technological leaders have better skills to compete than traditional companies.

The same is true in the financial industry, where banks no longer compete solely with other banks, but compete against telephone companies, which, by popularizing smartphones, began to invade the money transfer and remittance market abroad. Banks are also concerned about financial startups, also known as fintechs that evolve 10 times faster than a traditional bank to launch new products and services.

To understand this phenomenon, just ask yourself what business competes Amazon, which today, in addition to being the undisputed leader of e-commerce, has entered into areas such as digital book readers (Amazon Kindle), digital services in the cloud (Amazon Web Services), banking services, retail, health, among others.

Amazon Business Portfolio in 2018

In an environment where the boundaries between industries are blurred and the barriers to entering an industry are getting smaller – thanks to new digital technologies that make physical assets irrelevant and competitive advantages obsolete -, it is a mistake for companies to continue using industry as a unit of analysis.

The new unit of analysis should be the “arenas”, which are playing fields where several industries are located and present opportunities to enter new markets, in a broader view of the competitors than what is currently being taken into account in their strategic plans.

In fact, 65% of executives anticipate greater convergence between industries in the coming years and 54% expect more competition from other industries, that is, digital invaders with different business models, or what has come to be known as the “uberization” of their companies. industries. (IBM [13])

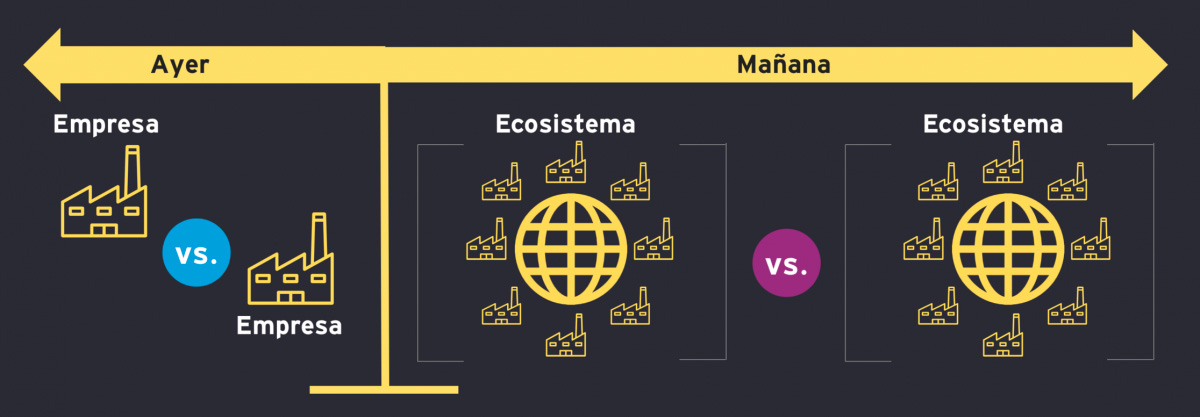

Due to the reduction of barriers between industries, in the future the value will migrate to different places in a redefined industry, where it will be key for companies to develop their competitive advantage through participation in ecosystems.

We will no longer see companies competing against companies, but allied ecosystems against allied ecosystems, where the unit of analysis will not be your industry; will be the new arenas of opportunity.

Do not consider digital transformation in strategy development

Today, digital technologies are both an opportunity and a threat to all companies. An opportunity for digital technologies to develop new capabilities to automate their value chains and reduce costs and, on the other hand, open new distribution channels to play in, such as e-commerce.

Companies should not think of digital transformation as something that applies only to the digital market or e-commerce, but rather as a capacity that has enormous potential such as process innovation and the creation of new business models. However, these technologies also pose a threat, as companies that do not adopt may be left behind.

The high penetration of companies like Uber in Latin America and the recent announcement that Amazon is starting to make direct deliveries in some Latin American countries and opening distribution centers in Mexico and Chile, for example, have made many entrepreneurs wonder if it really is. the belief that new technologies penetrate the most developed countries first and then slowly reach our markets is correct. The digital theme is growing in priority on the companies’ agenda. However, many executives admit they do not understand, let alone know how to manage.

Worldwide, 95% of the executives surveyed believe that the digital strategy should be incorporated into the business strategy, and that digitization is ranked as the disruptor with the greatest potential for companies. On the other hand, less than 25% feel completely prepared to face it (A.T. Kerney).

It is predicted that by 2020 more than 50% of company tickets will come from digital channels or digital products, services and businesses (AT Kerney), and that 66% of executives expect greater personalization of interactions with their customers through technology ( IBM Global C-Suite Study). Among respondents, 50% believe that digitization will have a high or even transformational impact on their business, and 72% believe that the total digital impact will be felt in the next 2 to 5 years (A.T. Kerney).

Leaders who are defining their business strategy need to ask themselves the following questions about how the digital transformation will affect their company:

- How will my strategy give me a competitive advantage in the digital world?

- How does digital technology affect the configuration of my value chain and the activities required to compete?

- How will digital technology change the structure and boundaries of the industry?

- What kinds of strategic decisions about digital technologies should my company make today to gain a competitive advantage in the future?

- Which new sales channels will allow you to explore digital technology?

- How can I use technology to customize my products and services to the needs of each customer?

- What is the culture that my company needs to adopt digital technologies and the challenges that affect a successful implementation?

Not considering innovation within the strategic planning process

It has already been demonstrated that traditional strategic planning processes are no longer suitable for an increasingly uncertain and unpredictable world. Companies can no longer afford to design strategies that make small adjustments to compete in the present that produce incremental results. This makes it necessary to innovate in the company’s strategy (strategic innovation), create new business models and innovate to create new ways to differentiate itself (temporal advantages).

Today, strategy and innovation have become inseparable concepts. Innovation must be a key function of the strategy, so that it does not remain in the “exploration” of what exists today, if it also does not focus on the “exploration” of the company’s future. The formulation of the strategy went from being an analytical process to becoming a process that mixes analysis with creativity, to create new possibilities and future options.

Martin Reeves, in his book Your Strategy Needs a Strategy suggests that the approach of the classic strategy (positioning, scale, operational efficiency, etc.) is useful only for environments that do not change and are predictable, which are less and less common, since all industries face disruption.

About this, 93% of the executive segment consider that innovation is a key factor for their future success; however, only 36% believe they have the capabilities to innovate (Palladium). 81% are skeptical about their organization’s ability to develop new products and services that are strong enough to overcome threats from other players in the market (Palladium). 60% report that their value propositions are being challenged at the moment, and only 12% indicate that innovation is practiced in their companies in relation to the customer experience.

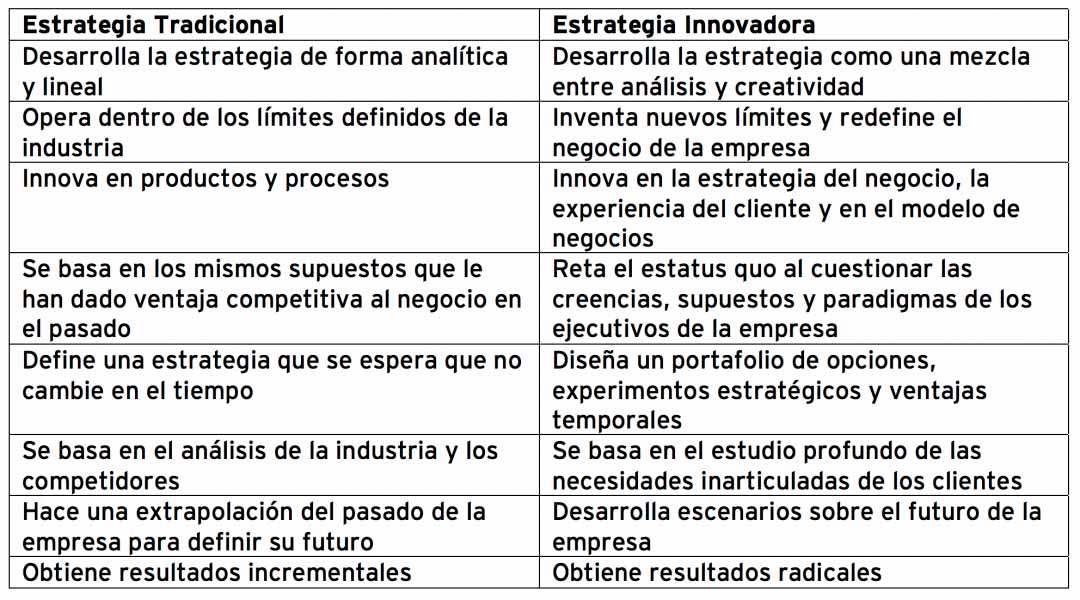

The following table shows the difference between a traditional strategy and an innovative strategy:

Recommendations for your company’s strategic planning

After analyzing the trends that affect companies’ planning processes, we propose the following suggestions for developing the strategic planning of the future:

- You need to see strategic planning as an ongoing journey and not an annual event

In a world that changes so quickly, it is a mistake to think that it is enough to review the strategy once a year. Companies must continually monitor their surroundings to detect whether any of the pillars on which their strategy is based are no longer valid. We recommend that strategic dialogues be held at least every quarter, to make strategic decisions in real time throughout the year and to have the ability to reallocate resources on opportunities that will bear fruit for the company, as well as take them out of businesses that do not. have a competitive advantage.

- Use the most up-to-date tools for the times we live in

Just as you would not allow a doctor to operate you with outdated tools, do not allow your company to use obsolete tools for the new context you face on a daily basis. We suggest abandoning outdated tools such as SWOT and replacing them with more modern ones such as Future-Back analysis, Strategic Cascade, visual strategic planning and the use of arenas of opportunity instead of industry, as a strategy analysis unit.

- Follow a planning process that guarantees decision making

Avoid falling into the trap of believing that a plan or a budget is the same as a strategy. Empower your entire team on what is the fundamental essence of the strategic planning process, which consists of making choices and, therefore, making waivers. Company employees are tired of running in all directions, trying to “boil the whole ocean”, the cause of strategies that do not waive and produce mediocre results in the organization’s financial performance.

- Incorporate digital strategy into business strategy

Today, digital strategy cannot be separated from business strategy. Both the business strategy gives direction to the digital strategy and the digital strategy gives new capabilities to the business strategy. Integrate both processes so that your company has a competitive advantage and that the digital transformation supports your business objectives.

- Incorporate innovation into your strategic planning process

Currently, it is not possible to design a winning strategy without innovation. Incremental strategies are not enough to survive in a world that changes exponentially. Incorporate innovation into your strategic planning process so that you can develop strategies to extend the life of your current business model, as well as help you explore new business models where your company’s future revenue will come from.

Conclusion

Companies that aspire to survive in the ultra-competitive context need to transform their strategic planning processes so that they are more continuous, agile and effective. Strategic planning processes need not be complex, large and tedious if the most modern tools are used and aligned with the times in which we live.

Referências

[1] VUCA em inglês (Volatile, Uncertain, Complex, Ambigous)

[2] Innosight: 2018 Corporate Longevity Forecast: Creative Destruction is Accelerating

[3] http://thepalladiumgroup.com

[4] KPMG Global CEO Study

[5] A.T. Kearney’s 2014 Strategy Study

[6] KPMG Global CEO Study

[7] http://thepalladiumgroup.com

[8] O índice Standard & Poor’s 500 (Standard & Poor’s 500 Index) também conhecido como S&P 500 é um dos índices acionários mais importantes dos Estados Unidos e é considerado o índice mais representativo da situação real de mercado.

[9] Transcient Competitive Advantage

[10] https://www.strategyand.pwc.com

[11] IBM Global C-Suite Study

[12] McKinsey Global Survey

[13] IBM Global C-Suite Study